(Bloomberg) — Asian stocks are poised to fall early Monday as concerns over the health of the Chinese economy grow. US equity futures were steady.

Most Read from Bloomberg

Contracts in Australia, Hong Kong and mainland China point to an early loss at the Monday open, while moves in Asia may be exacerbated by thin liquidity with Japanese markets closed for a holiday. The S&P 500 closed 0.2% lower on Friday following a quarterly options expiry.

Data late Friday showed Chinese governments have cut spending while the youth jobless rate climbed to its highest level this year as the nation’s banks refrain from cutting lending rates. Adding to the weak sentiment, the US is said to be planning rules that would ban Chinese hardware and software for connected vehicles as soon as Monday.

“Things in China are going from bad to worse,” said Tony Sycamore, an analyst at IG in Sydney. “With Japanese stock markets closed for a public holiday, the PBOC disappointing the market on Friday, and US yields ratcheting higher, we are likely to see a more downbeat tone across Asian equity markets today.”

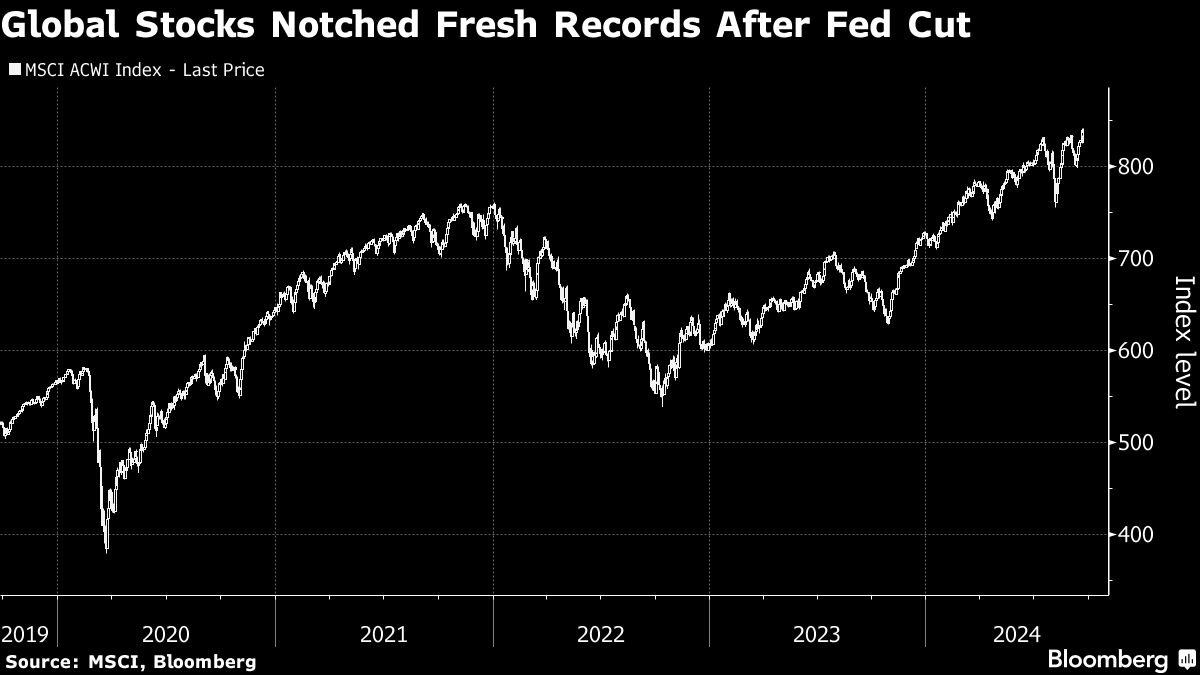

Broadly, markets are readying for the final quarter after the Federal Reserve began its long awaited rate cut cycle last week, lifting everything from Indonesian bonds to gold. Data this week including the Fed’s preferred measure of inflation should confirm whether the rally will extend, with a deterioration likely lifting odds of a further 50 basis point cut.

After wavering between gains and losses in the final minutes of Friday trading, the S&P 500 and Nasdaq 100 both closed lower with the broader benchmark fresh off its 39th record high of 2024. The blue-chip Dow Jones Industrial Average closed at a new record. More than 20 billion shares changed hands on US exchanges, the busiest session since January 2021.

Intel Corp. was among the session’s advancers after reports of a bid by Qualcomm Inc. Shares may extend gains in US trading after Apollo Global Management Inc. was reported to offer to make an equity-like investment of as much as $5 billion in the chipmaker.

Gold closed above $2,600 an ounce on Friday, extending gains after an Israeli strike on a Beirut suburb. The precious metal and oil were steady in early trading as Hezbollah launched retaliatory attacks toward vast areas of Israel’s north after the pager and other electronic device explosions last week that killed at least 39 people in Lebanon.

The dollar was little changed against major peers early Monday. Cash trading of US Treasuries was closed in Asia due to the holiday in Japan. Australian bonds fell ahead of the central bank likely extending a policy pause on Tuesday as housing costs underpin sticky inflation.

“Our Australian economics team expect the RBA’s comments to be hawkish, albeit marginally less hawkish than in August, helping guide the Australian dollar higher,” Commonwealth Bank of Australia strategists including Joseph Capurso wrote in a note to clients. “Quite a bit needs to go right for the RBA to cut the cash rate this year; the risk is a delay into early 2025.”

Elsewhere this week, factory activity and consumer confidence readings in Europe are due while Australia and Tokyo are set to release inflation data. A swath of Fed speakers are due as economic data including the US personal consumption expenditures gauge and jobless claims are scheduled to be released.

Key events this week:

-

Malaysia CPI, Monday

-

Eurozone HCOB Manufacturing PMI, HCOB Services PMI, Monday

-

UK S&P Global Manufacturing PMI, S&P Global Services PMI, Monday

-

Australia rate decision, Tuesday

-

Japan Jibun Bank Manufacturing PMI, Services PMI, Tuesday

-

Mexico CPI, Tuesday

-

Bank of Canada Governor Tiff Macklem speaks, Tuesday

-

Australia CPI, Wednesday

-

China medium-term lending facility rate, Wednesday

-

Sweden rate decision, Wednesday

-

Switzerland rate decision, Thursday

-

ECB President Christine Lagarde speaks, Thursday

-

US jobless claims, durable goods, revised GDP, Thursday

-

Fed Chair Jerome Powell gives pre-recorded remarks to the 10th annual US Treasury Market Conference, Thursday

-

Mexico rate decision, Thursday

-

Japan Tokyo CPI, Friday

-

China industrial profits, Friday

-

Eurozone consumer confidence, Friday

-

US PCE, University of Michigan consumer sentiment, Friday

Some of the main moves in markets:

Stocks

-

S&P 500 futures were little changed as of 8:23 a.m. Tokyo time

-

Hang Seng futures fell 0.5%

-

S&P/ASX 200 futures fell 0.8%

Currencies

-

The Bloomberg Dollar Spot Index was little changed

-

The euro was little changed at $1.1163

-

The Japanese yen was little changed at 143.82 per dollar

-

The offshore yuan was little changed at 7.0442 per dollar

-

The Australian dollar was little changed at $0.6806

Cryptocurrencies

-

Bitcoin rose 0.4% to $63,486.59

-

Ether rose 0.1% to $2,576.21

Bonds

Commodities

This story was produced with the assistance of Bloomberg Automation.

Most Read from Bloomberg Businessweek

©2024 Bloomberg L.P.

Source link